Statement of Financial Position

Cornell’s Balance Sheet

The Statement of Financial Position, often called the balance sheet, records Cornell’s assets, liabilities, and net assets on a given date.

What We Own: Cornell’s Physical and Non-Physical Assets

Assets largely include investments; land, buildings, and equipment; accounts receivables; and cash.

Cornell's most significant assets are investments, receivables, and capital assets including land, buildings, equipment and other tangible assets.

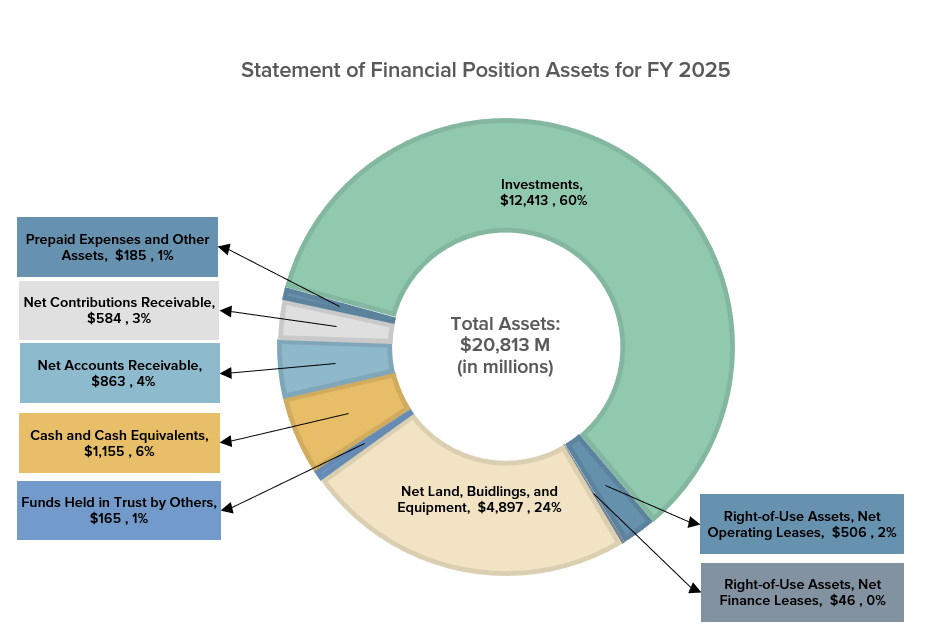

Statement of Financial Position Assets table

Cash and Cash Equivalents

Amount: $1,155M (FY 2025)

This amount includes cash on hand and in bank accounts, money market funds, and other temporary investments held for working capital purposes with an original maturity term of ninety days or less.

The carrying amount of cash equivalents approximates fair value because of their short terms of maturity. Cash that is part of the university’s investment portfolio is reported as investments.

Net Accounts Receivable: Amounts Due to Cornell from Others

Amount: $863M (FY 2025)

Net accounts receivable represents amounts due from others for:

- Outstanding accounts that are due to the university, primarily due from federal, state, and private sponsors (for research), patients (for medical services), commercial third parties, students (for tuition and fees), and promises made by donors to contribute to the university.

- Outstanding federal Perkins and Health Professions loans as well as university loans issued to students while attending Cornell and Weill Cornell Medicine, net of allowances for doubtful accounts. The Student Loan Repayment and Collections department performs billing, servicing and collections for these loans and processes all related deferments and payments.

| Summary of Accounts Receivable | 2024-2025 |

|---|---|

| Grants and Contracts | $255,763 |

| New York-Presbyterian Hospital and Other Affiliates | $129,319 |

| Patients (net of price concessions and bad debt allowances) | $126,766 |

| Reinsurance Receivable | $200,905 |

| Federal Revolving Student Loans | $5,128 |

| Institutional Student Loans | $25,079 |

| Student Accounts | $34,120 |

| Other | $86,252 |

| Net Accounts Receivable | $863,332 |

Net Contributions Receivable: Gifts Due to Cornell

Amount: $584M (FY 2025)

Net contributions receivable represents pledged receivables that are due to the university, net of allowances for doubtful accounts.

A pledge is an agreement between a donor and the organization where the donor promises to contribute, at a later date, cash or other assets to the organization.

To qualify as a pledge, the university must confirm that the donor has made a firm commitment and that the pledge is unconditional.

| Summary of Contributions Receivable | 2023-2024 |

|---|---|

| Less than One Year | $280,667 |

| Between One and Five Years | $325,276 |

| More than Five Years | $47,165 |

| Gross Contributions Receivable | $653,108 |

| Less: Unamortized Discount | $-51,155 |

| Less: Allowance for Uncollectible Amounts | $-18,059 |

| Net Contributions Receivable | $583,894 |

Prepaid Expenses and Other Assets

Amount: $185M (FY 2025)

This amount represents future expenses that have been paid in advance.

Examples of these expenses are insurance, software licenses, and rent.

Investments

Amount: $12,413M (FY 2025)

This amount consist of funds held as long-term investment (LTI), separately invested (SI), and other investments.

The LTI is managed by the Office of University Investments and represents approximately 95% of total investments. The long-term investment pool (LTIP) owns shares in the LTI and represents about 95% of the LTI or 90% of total investments.

Investments are recorded at fair value and consist of the historical value plus or minus investment returns (income, realized and unrealized gains/losses) less LTIP withdrawals approved by the Board of Trustees.

Long-Term Investment Pool (LTIP)

The LTIP:

- Functions much like a mutual fund, whereby participants buy shares at the current market value share rate and receives a per-share annual income payout as determined by the Board of Trustees.

- Is funded by true endowment contributions received by donors and funds functioning as endowments (FFE), and funds held for others.

An FFE is also known as a Quasi endowment. An FFE:

- Functions similar to a true endowment but the principal amount may be totally expended at any time.

- May include unrestricted gifts along with college and department excess fund balances that maybe invested in the LTIP for a minimum of five years.

True endowments gifts stipulates that the principal amount is not expendable (invested in perpetuity).

Investment Policy

The Investment Committee is responsible for the investment policy. Cornell’s investment objective for its endowment assets is to maximize total return within reasonable risk parameters, specifically to achieve a total return, net of expenses, of at least 5% in excess of inflation, as measured by the Consumer Price Index over rolling five-year periods.

The achievement of favorable investment returns enables the university to distribute over time increasing amounts from the endowment so that present and future needs can be treated equitably in inflation-adjusted terms.

Diversification is a key component of the university’s standard for managing and investing endowment funds, and asset allocation targets are subject to ongoing reviews by the Investment Committee of the Board of Trustees.

University Endowment

Cornell’s endowment was established predominantly with money or other financial assets donated to the university. The university intends that the endowment be invested in such a way that it increases in value while generating enough income to support the university’s mission.

Donor-restricted (true) endowment funds must be held in perpetuity and the university may only spend a portion (as determined by the Board of Trustees) of the earnings from the investments. The university has also made strategic decisions to invest additional funds in its endowment to provide long-term financial stability.

Types of Gifts

- Cash contributions: Donations received in the form of cash.

- Gifts to endowment: Permanently restricted gifts.

- Bequests: Property or money pledged to be provided after the donor passes away.

- Pledges: Promises to donate property or money at a later date.

- Unrestricted gifts: Gifts without donor restrictions.

- Temporarily restricted gifts: Gifts with donor restrictions that can be removed if donations are used in a certain way or by the passage of a certain amount of time.

- Permanently restricted gifts: Gifts with donor restriction stating that the principal of the gift cannot be touched.

How Investments Grow

The underlying security holdings within the LTI are managed by numerous external investment managers, selected and engaged with by the Office of University Investments on behalf of the university and held in discreet investment portfolios by manager.

Investment earnings (income, realized and unrealized gain/loss) experienced in these portfolios are based on the associated investment activity (valuation changes, asset sales, dividends, etc.) within the manager portfolios.

Investment earnings are allocated by Bank of New York Mellon to the six LTI plan accounts (buckets within the LTI) based on the number of LTI shares (Master Trust Units) that each plan account holds.

Investment earnings are reflected on the monthly investment statement and posted to investment returns – net of amount distributed on the financial statement line.

LTIP net investment earnings (income and realized/unrealized gain/loss less LTIP withdrawal) are allocated to each LTIP account based on the number of LTIP units that the individual account holds.

Right-of-Use Assets, Net Operating and Finance Leases

Net Operating Leases Amount: $506M (FY 2025)

Net Finance Leases Amount: $46M (FY 2025)

These amounts represent the values of assets Cornell has the right to use over the life of leases. A finance lease transfers ownership of the asset to Cornell at the end of the lease term, or Cornell consumes most of the economic value of the asset during the lease term. An operating lease is treated more like renting.

Net Land, Building, and Equipment

Amount: $4,897M (FY 2025)

This amount represents the acquisition amount of land, buildings, and equipment, net of accumulated depreciation.

These are physical, tangible assets expected to generate economic benefits for the institution for a period greater than one year.

| Net Land, Buildings, and Equipment | 2024-2025 |

|---|---|

| Land, Buildings, and Equipment | $7,753,084 |

| Furniture, Equipment, Books, and Collections | $1,781,593 |

| Construction in Progress | $861,401 |

| Total before Accumulated Depreciation | $10,396,078 |

| Accumulated Depreciation | $-5,499,121 |

| Net Land, Buildings, and Equipment | $4,896,957 |

Funds Held in Trust by Others

Amount: $165M (FY 2025)

These are funds for which the university acts as a custodian, trustee, manager, or agent but over which it does not exercise control.

What We Owe: Cornell’s Debts or Liabilities

Liabilities include expenses incurred but not yet paid such as accounts payable, payroll, debt, and medical and pension benefits.

Cornell's most significant liabilities are debt incurred to fund building and maintaining facilities, payments due for goods and services, and deferred benefits.

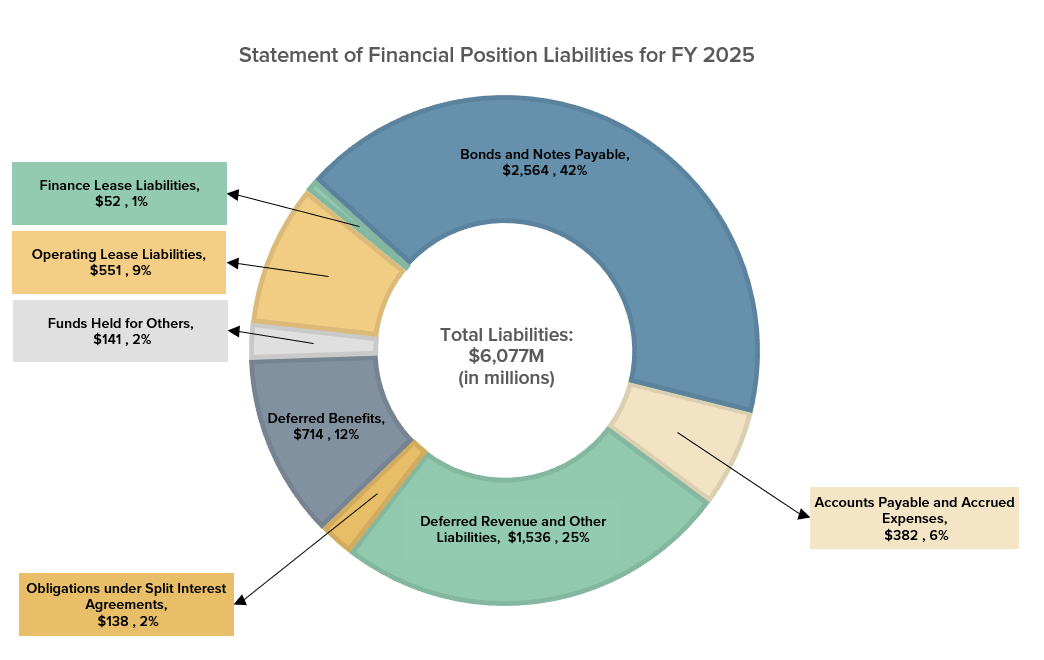

Statement of Financial Position Liabilities table

Accounts Payable and Accrued Expenses: Amounts Due for Goods and Services

Amount: $382M (FY 2025)

Accounts payable are payments due, generally within 90 days, for goods or services purchased on credit.

Accrued expenses are reported in the period in which they occur, but payment is made in a subsequent period.

The vast majority of the university's accrued expenses are salaries and benefits earned but not paid as of the end of the fiscal year.

Deferred Revenue and Other Liabilities

Amount: $1,536M (FY 2025)

This amount represents payments received in advance for services not yet performed or goods not yet delivered, including funds owed to the government by the university for student loans.

An example of deferred revenue is summer session tuition collected for the summer but not earned until the summer session instruction has been provided.

Obligations Under Split Interest Agreements

Amount: $138M (FY 2025)

Split interest agreements are contributions that assign to the university and other beneficiaries the legal rights to certain assets.

The portion of the assets assigned to the other beneficiaries is the amount of the obligation or liability.

Deferred Benefits: Employee Benefits Payable

Amount: $714M (FY 2025)

This amount includes benefits to employees that are not yet paid.

The largest component is the obligation the university has to its employees after retirement, including pensions and retiree health and life insurance benefits.

Other significant benefits include vacation accruals, deferred compensation, and medical benefit claims incurred but not yet reported.

Retirement

Cornell’s employee retirement plan coverage is provided by two basic types of plans: one based on a predetermined level of funding (defined contribution), and the other based on a years-of-service calculation to determine the level of benefit to be provided (defined benefit).

The primary defined contribution plans for endowed colleges at Ithaca and for exempt employees (those not subject to the overtime provisions of the Fair Labor Standards Act) at Weill Cornell Medicine (WCM) are carried by the Teachers Insurance and Annuity Association and Fidelity Investments (endowed colleges) only, all of which, all of which permit employee contributions within the tax deferred annuity plans.

All except non-exempt staff members at WCM are included in the defined contribution plan.

WCM maintains Cornell’s only defined benefit pension plan, available only to nonexempt employees at WCM who meet the eligibility requirements.

The plan was frozen in 1976 for exempt employees at WCM and the accrued benefits were merged with the active nonexempt retirement plan in 1989.

In accordance with Employee Retirement Income Security Act (ERISA) requirements for the defined benefit plans, the university must fund annually with an independent trustee an actuarially determined amount.

Defined Contribution vs. Defined Benefit

With a defined benefit plan, most often known as a pension, the university completely funds and promises a set payout when the employee retires.

With a defined contribution plan, such as a 401(k) or 403(b), the university and the employee can contribute on a regular basis. The future benefits to the employee fluctuate on the basis of investment earnings.

Funds Held for Others

Amount: $141M (FY 2025)

This amount represents funds invested on behalf of related organizations.

Independent trustees are responsible for the designation of income distribution.

Operating and Finance Lease Liabilities

Operating Lease Amount: $551M (FY 2025)

Finance Lease Amount: $52M (FY 2025)

This amount includes funds owed by the university for the use of real estate and buildings. A finance lease transfers ownership of the asset to Cornell at the end of the lease term, or Cornell consumes most of the economic value of the asset during the lease term. An operating lease is treated more like renting.

All leases for equipment are immaterial.

Bonds and Notes Payable

Amount: $2,564M (FY 2025)

This amount represents obligations held by the university resulting from money borrowed from investors or banks.

These are normally used to fund building construction or improvements.

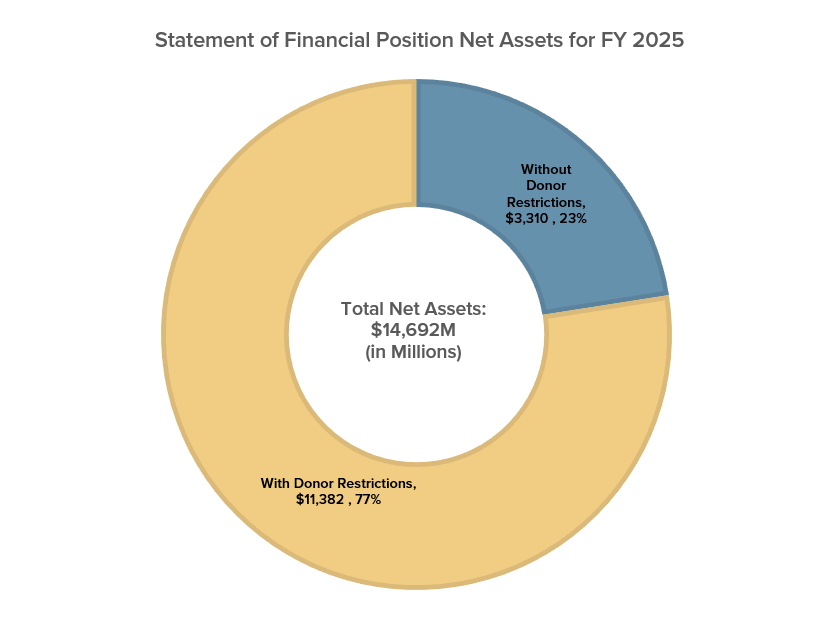

Our Net Worth: Cornell’s Net Assets

Net assets make up the difference between assets and liabilities and are classified with or without donor restrictions.

Net assets is made up of the endowment (money or other financial assets donated to Cornell), investment physical capital assets like the campus buildings and equipment, and other net assets such as operating balances, funds available for student loans, and funds held by others that will eventually benefit Cornell.

Statement of Financial Position Net Assets table

Net Assets without Donor Restrictions

Amount: $3,310M (FY 2025)

This amount represents assets donated without limitations or restrictions except that the funds must be used by a particular college or department.

Net Assets with Donor Restrictions

Amount: $11,382M (FY 2025)

This amount represents donated assets that either:

May be used only after a specified period of time or only for a specific purpose, or both. The restriction is satisfied either by the passage of time or by actions of the organization.

OR

Will be maintained permanently or invested in perpetuity and assets. Permanent restrictions can never be removed by actions of the organization, although the restriction can be removed by court order. Generally, only true endowments are included.